Designing a clearer path for declined customers

When a customer is declined for term life insurance, the moment can feel like a dead end. I led the end-to-end design of an embedded Guaranteed Issue experience – turning a disappointing "no" into a clear, next step.

Role

Lead Product Designer

Timeline

2026

Scope

End-to-end – research to execution

Focus

Research, workshops, UX flows, messaging

A decline shouldn't feel like a dead end

At PolicyMe, roughly about 15% of completed Term Life insurance applications were being declined or postponed, with especially higher rates among seniors due to health and other risk factors. We had no PolicyMe-branded alternative, which mean sending these customers to an external agent for coverage. This broke our "one-stop-shop experience" and weakened our value of "never say no" and left brand value and business on the table.

The challenge was to build a standalone and embedded Guaranteed Issue Life Insurance journey that could give these customers a credible path to purchase coverage that still provides them with peace of mind for their loved ones.

Designing the full cycle

I was responsible for shaping the experience for 2 journeys from end to end which included:

Understanding the customer problem

Facilitating early workshops with internal stakeholders and cross-functional teams to align on the problem space

Exploring different UX and messaging directions

Refining the solution based on feedback

Helping define a clearer path from decline to Guaranteed Issue

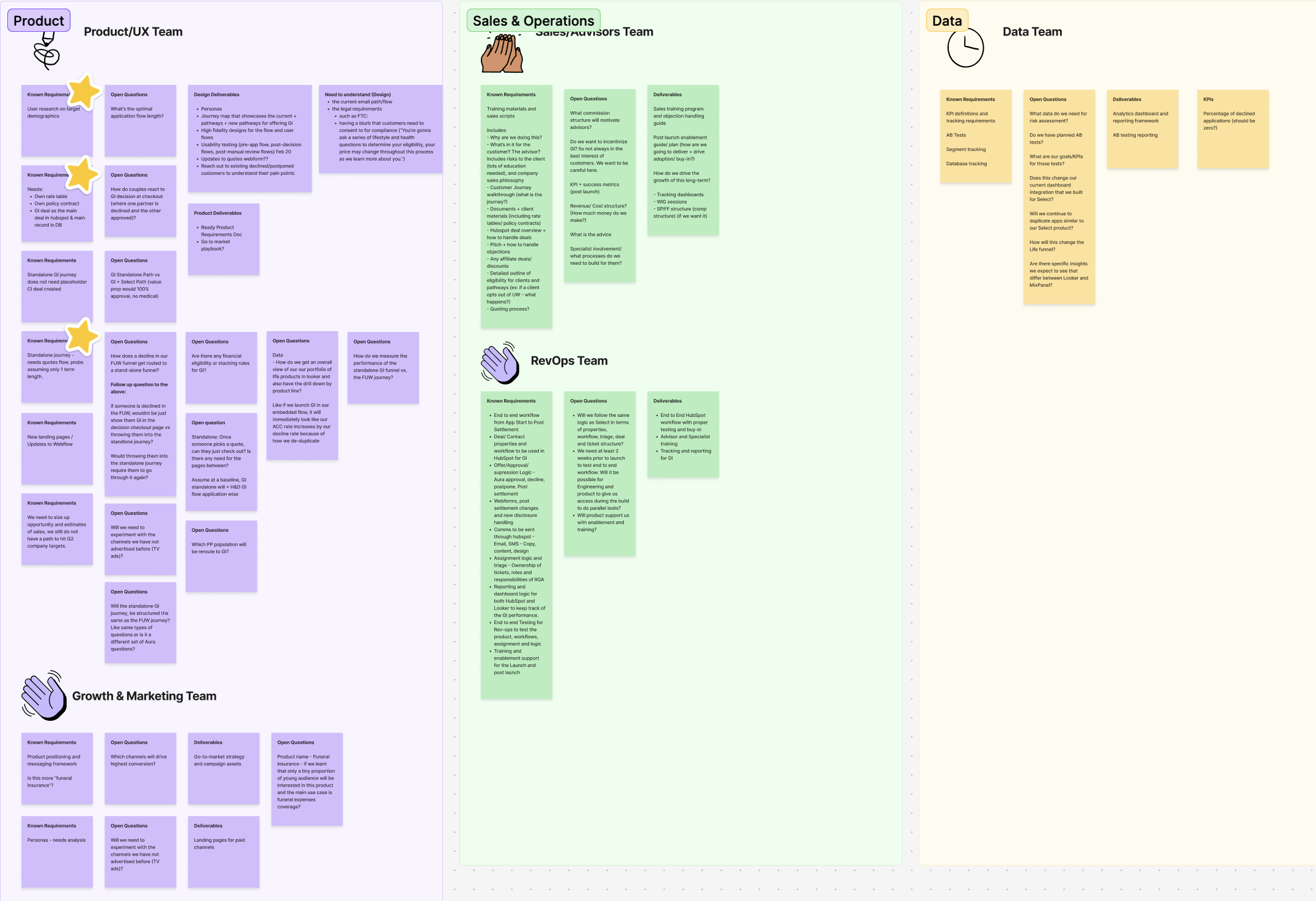

Bringing stakeholders in early

A new insurance product reaches across the whole company, not just the screens. I ran a series of 2-3 workshops; the first one was meant to capture requirements from every team that touches the journey. I brought each team to the same board to map what known requirements, open questions and deliverables.

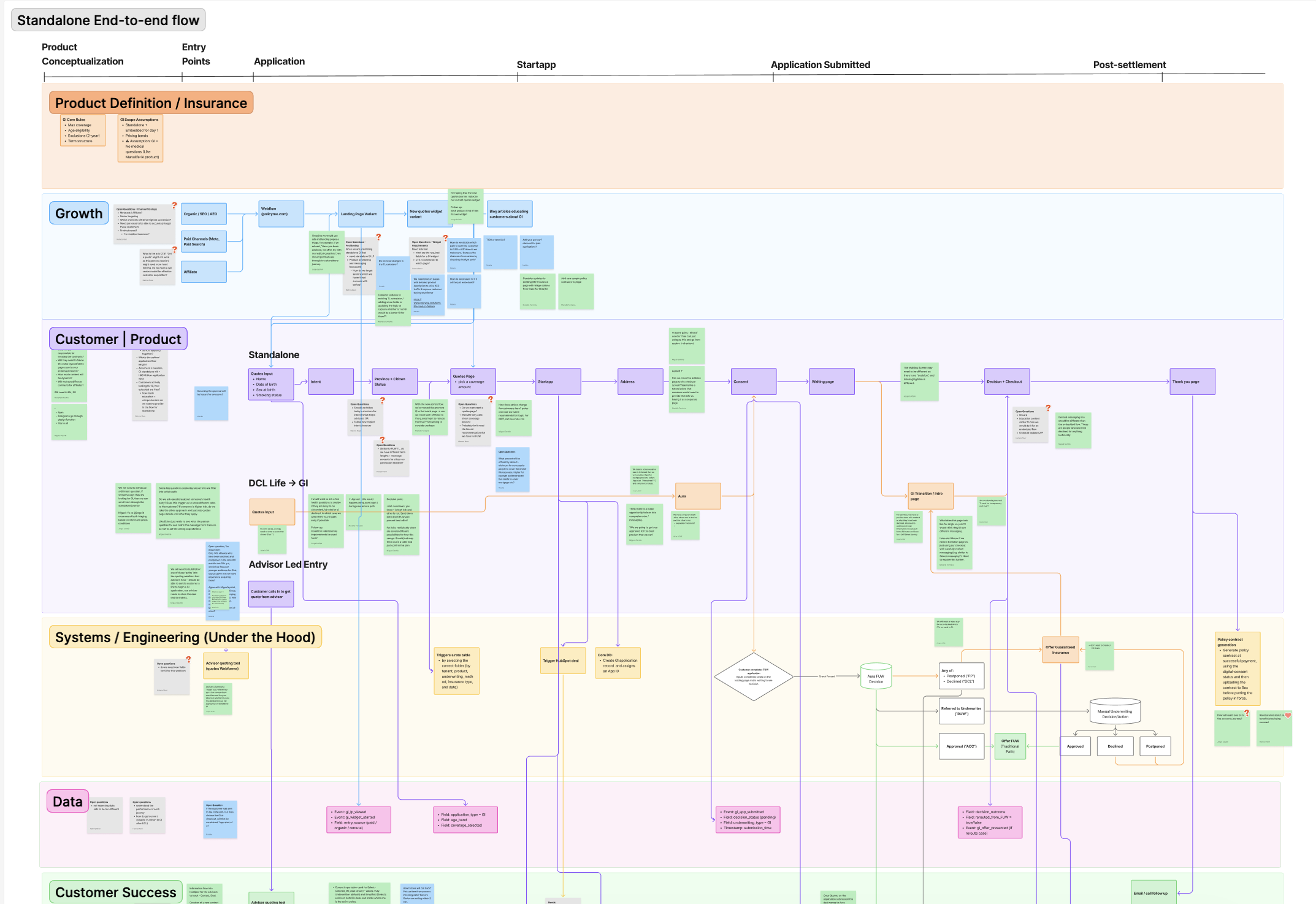

Mapping the end-to-end flow

I took all the insights from the workshop and began to draft a journey map that reflected my understanding of how the end to end flow could work across all cross functional teams. Of course there were areas where there were gaps in my knowledge and the 2nd workshop was used to to surface them.

Talking to the people closest to the customer

It was very integral that I spoke with advisors since they are our front lines. There were a few key questions that I wanted to answer including:

How advisors handle declined and postponed applications; language they use, what works or doesn't work with these cases

How customers actually react when they're told they have been declined for term life insurance

How we could offer Guaranteed Issue Life insurance as an alternative path without it feeling like a bait-and-switch

Here's what I learned

How the customer feels

Disappointment

Frustrated when given a generic reasoning

Anger is apparent when customers think its not fair (BMI)

How to handle a decline

Empathize

Explain that it's an industry standard, they can expect the same result at different companies

Share next steps like offering an external solution instead

How to frame GI differently

Need more explanation on the price gap

Connect back to their intent of getting insurance

Ask medical questions upfront to filter out GI customers

GI insurance needs and perceptions

As a part of launching this product, we needed to understand people's motivations and how they perceive life insurance and related needs later in life. We spoke to 2 cohorts; PolicyMe and external of people aged 55-75 for a total of 30 interviews total.

Here's what we learned

What drives people to act

New mortgage

Loss of employer coverage

Approaching retirement

Family health events

Watching a family member go without insurance

Product awareness and understanding

Product literacy is low, even among financially sophisticated participants. Misconceptions include:

Expecting GI products to include cash value

Not understanding the difference between various life insurance products (whole life, term life, etc)

Confusing GI benefits with government programs

Trust

GI products face a fundamental credibility problem, because there are no medical or health questions being asked

Jargon and speed are interpreted as deliberate manipulation – have to explain the product in simple terms

Price sensitivity is important - users wanted straightforward coverage

Principles that guided the designs

01

Lead with empathy

Meet people where they are. Whether they arrive directly or after a Term Life decline, the tone has to emulate the way an advisor would handle it with a human touch.

02

Be clear about what happens next

The next step cannot feel vague. People need a strong sense of what Guaranteed Issue is, why it's a better fit for them and how to continue to get peace of mind.

03

Position the alternative with intention

Guaranteed Issue Life Insurance shouldn't read as an afterthought, its often times a much simpler route to getting coverage for end of life expenses.

04

Building confidence toward their decision

Buying coverage is a real commitment. We needed to help the customer feel confident about the coverage they were purchasing.

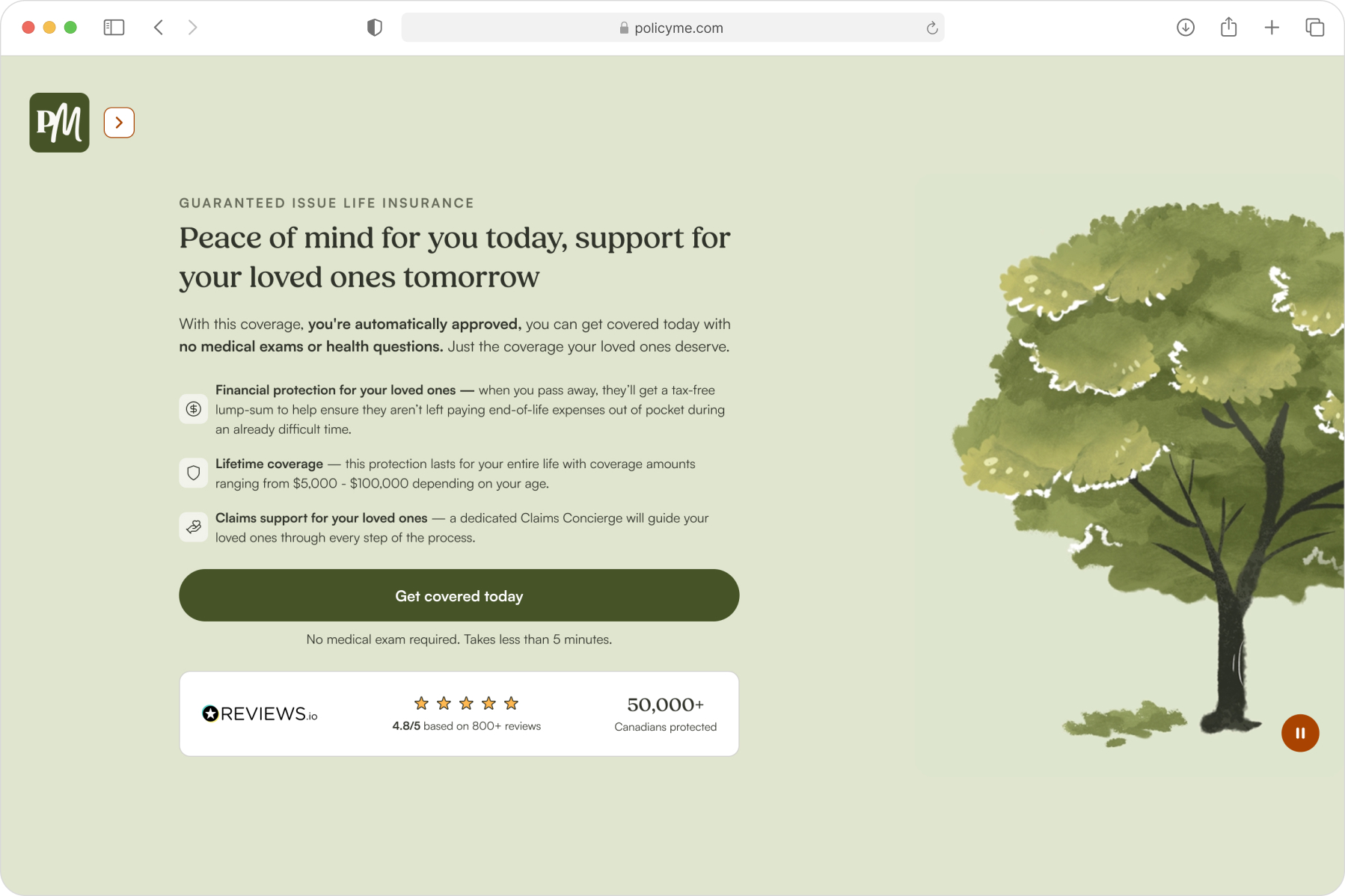

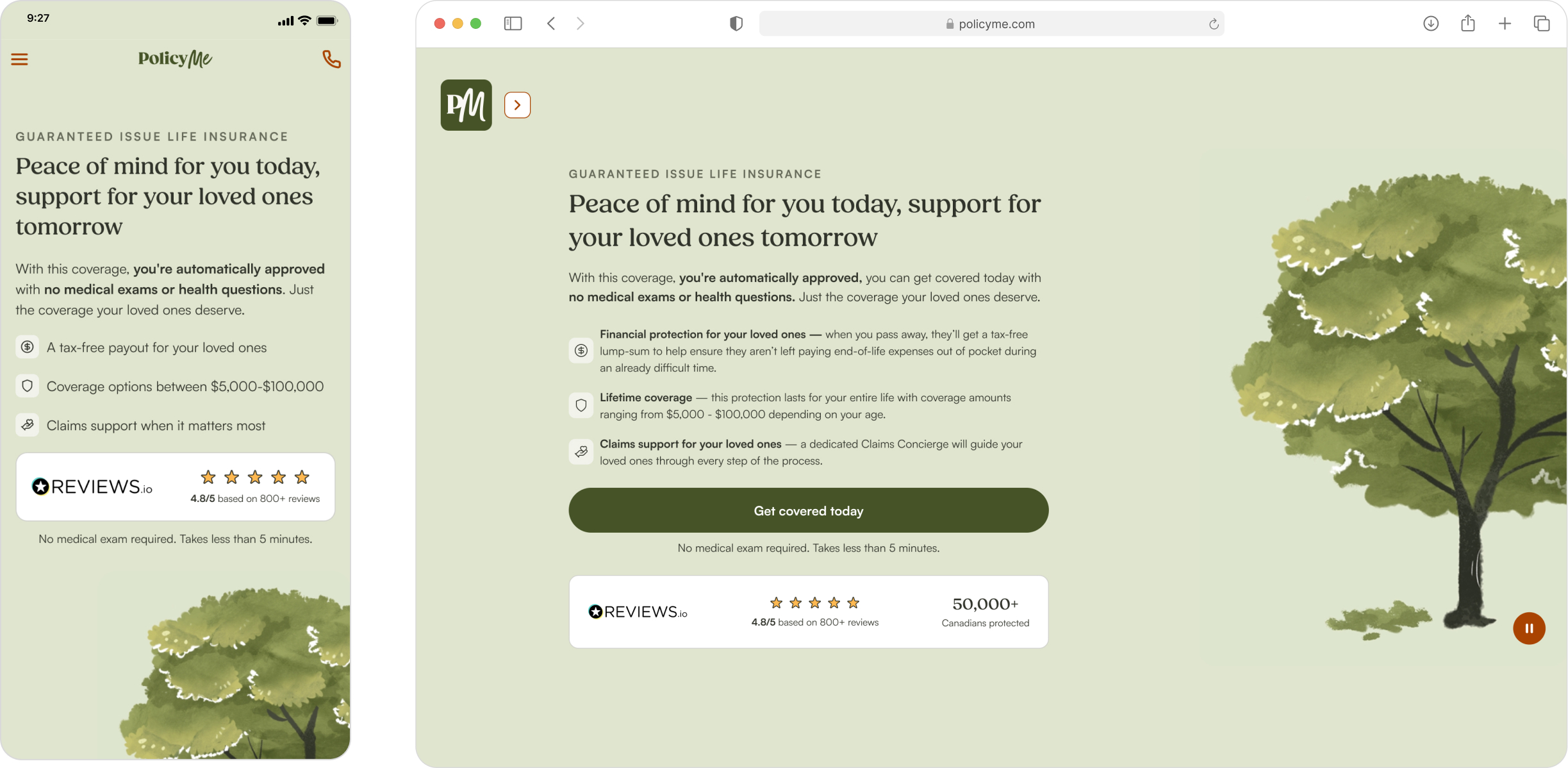

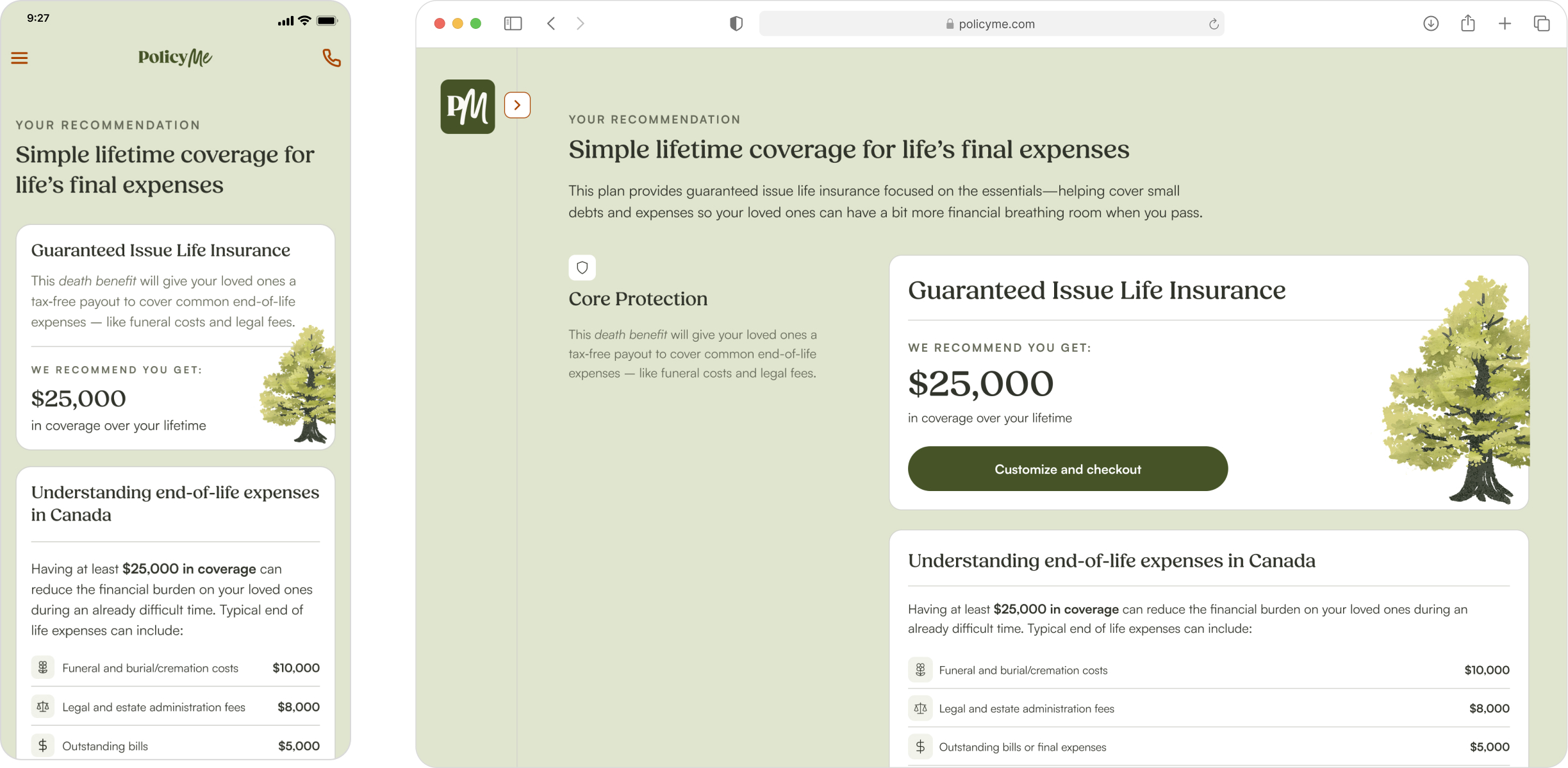

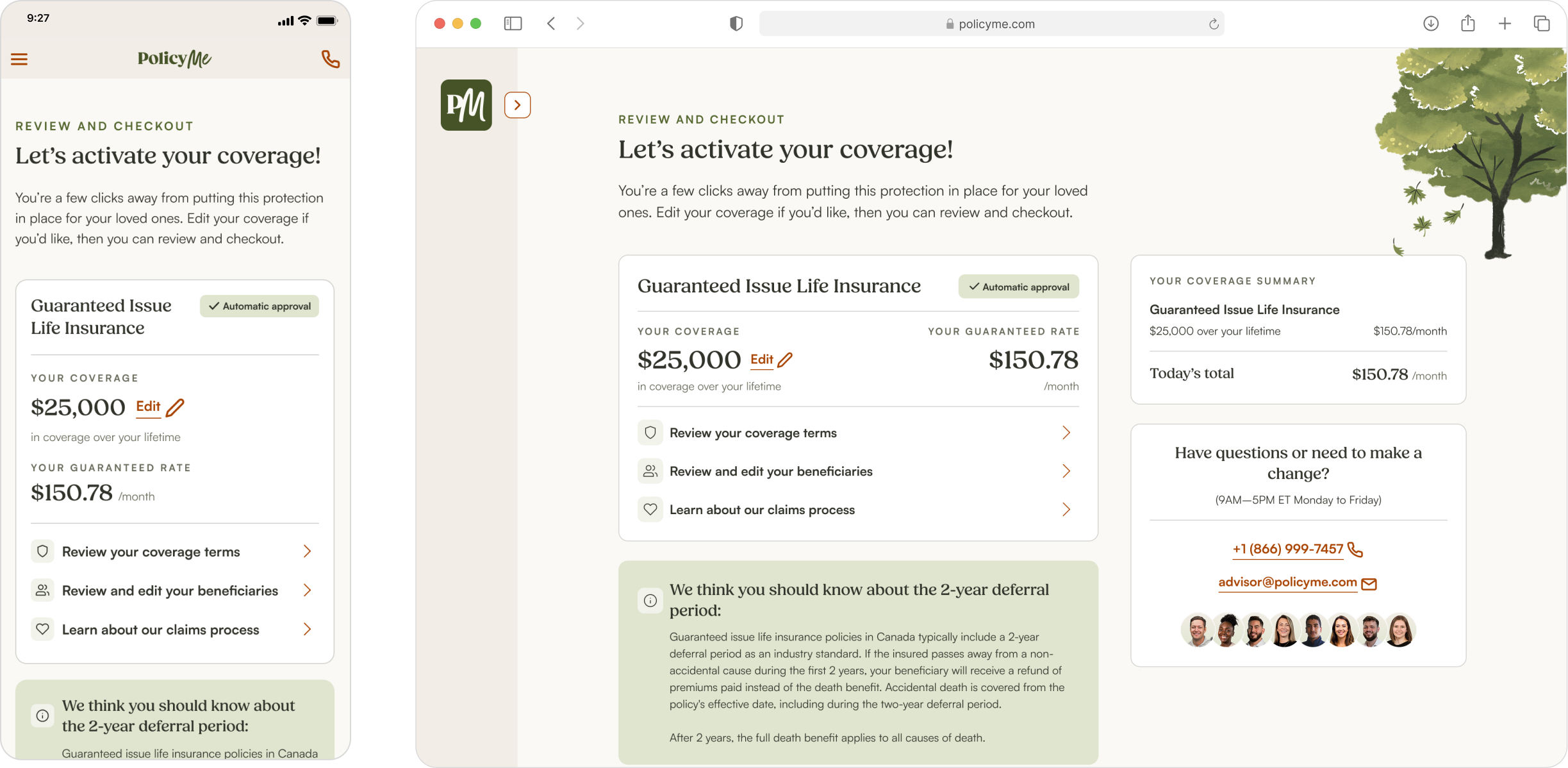

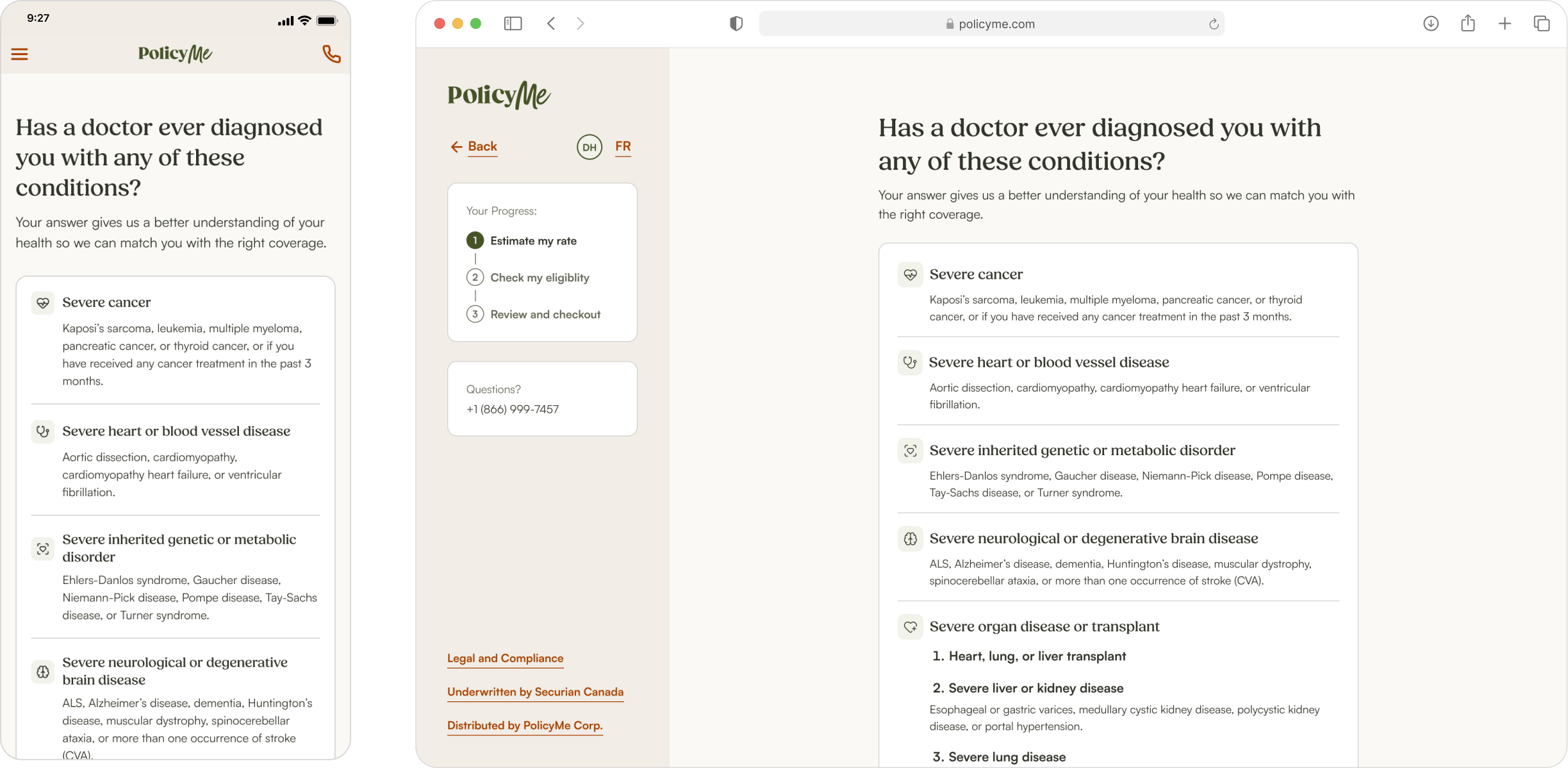

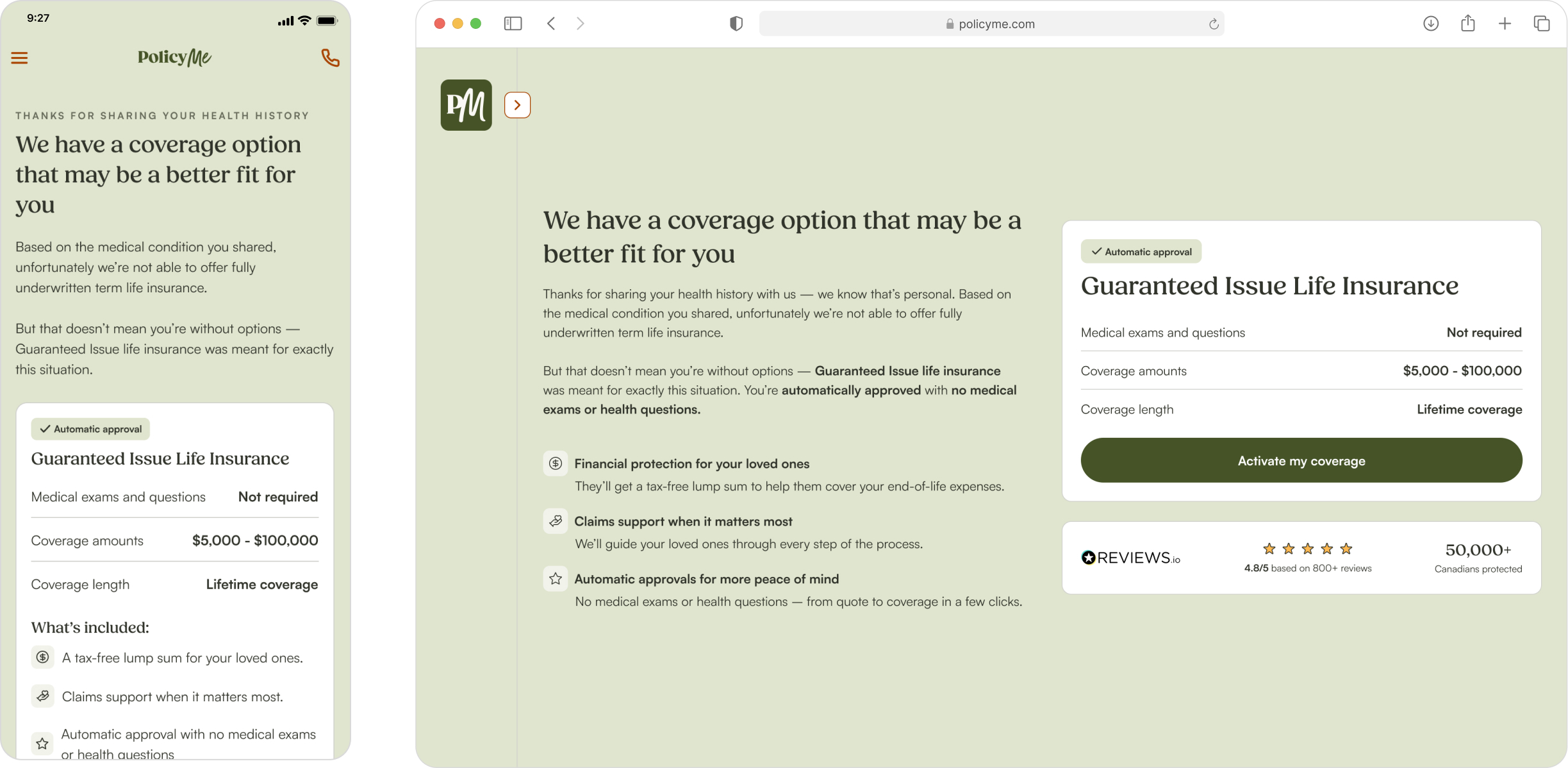

Standalone flow key screens

Embedded flow screens

Post launch reality

Customers were reaching checkout, but they weren't settling, so conversion was a lot lower than expected. We also saw low app-start to policy-create performance pointing to friction both before and at checkout.

The working hypothesis was that there is price shock at checkout, a moment that needed human reassurance

This opened up for a border opportunity – for a product of this nature, we need a clearer advisor touchpoint which could help the customer cross the finish line

This shifted how I though about the problem, it wasn't only about a clearer digital path, it was about recognizing where a fully self serve experience wasn't enough.

What I learned

This project challenged me to think across product, marketing, education, messaging and behaviour. I learned how valuable it is to:

frame a new product opportunity clearly

align stakeholders early through workshops and shared problem definition

design for both comprehension and conversion

recognize when a better product experience may require both digital and human touchpoints

The embedded journey actually surprised us, we had a couple customers who completed the application